Summary

Guyana’s net take inclusive of local content spend together with the government’s take cumulatively as of 2022 amounted to G$697.7 billion or US$3.34 billion representing 34.3% of the cumulative net operating cash flow for the period 2019-2022―which stood at G$2.033 trillion. Of this amount, the cumulative net cash flow transferred to the parent companies amounted to a meagre G$6.4 billion or US$30 million representing 0.31% of the cumulative net operating cash flows for the period.

The cumulative net cash flow of EEPGL, HESS and CNOOC for the period 2019-2022 revealed that Guyana earned a total of G$424 billion or US$2 billion cumulatively for this period which represents 21% of the cumulative net operating cash flows for the same period. Conversely, the oil companies have repaid a meagre G$6.4 billion or US$30 million to their parent companies which represents less than 1% of the cumulative net operating cash flows for the period FY 2019–FY 2022. Effectively, this means that the oil companies are reinvesting almost 100% of the net cash flows generated from the operating activities in Guyana in new exploration activities and to develop future projects into production.

This is especially important since there is a limited window in which to extract these resources in view of the global energy transition agenda that is likely to have an impact on global demand for crude and ultimately resulting in lower crude oil prices in the future. And equally, it is crucial for Guyana to maintain the current pace and momentum in the industry aimed at enabling the country’s sustainable economic transformation and development agenda.

1. Background

The financial analysis presented herein is a contextual analysis based on the consolidated audited financial statements for the financial year ended December 31, 2022, for Esso Exploration and Production Guyana Limited (EEPGL), Hess Guyana Exploration Limited (Hess), and CNOOC Petroleum Guyana Limited (CNOOC).

The objective of this report is to bring clarity and context in respect of the financial results of the oil companies’ activities in Guyana’s emerging petroleum industry. There have been several media reports on the local subsidiaries’ financial results wherein, for example, the gross earnings was reported incorrectly as the net earnings.

It should be noted that the audited financial statements are prepared in accordance with International Financial Reporting Standards (IFRS). Therefore, in order to derive the net earnings for the oil companies and the government’s take accordingly, the reported earnings ought to be adjusted by applying the fiscal terms pursuant to the Production Sharing Agreement (PSA) that governs the Stabroek block.

For ease of reference, the fiscal terms are stated as follows:

i) 50/50 profit share,

ii) 75% cost recovery ceiling, and

iii) 2% royalty

The analysis also sought to illustrate a global perspective by comparing the local operator’s, namely EEPGL’s financial indicators relative to the parent company’s (ExxonMobil) global financial indicators. The results demonstrate the extent to which the net earnings in the Guyana market contributed to the global net earnings, assets, and net operating cash flow. This is an especially important perspective for the Guyanese stakeholders since many observers and analysts have propagated the view that the Guyana’s oil and gas earnings account for a substantial portion of the parent company’s global earnings. The findings confirmed that this is not the case at this point in time.

2. Discussion and Analysis

Crude Oil Production

Citing the National Budget Speech, 2023, the oil and gas sector is estimated to have expanded by 124.8% in 2022, with a total of 101.4 million barrels of oil produced, compared with 42.7 million in 2021. The Liza-Unity Floating, Production, Storage and Offloading (FPSO) began producing in early-2022, increasing the number of FPSOs currently producing to two platforms. In 2023, it is anticipated that a third FPSO, Liza-Prosperity, will commence production by the end of this year. With these three FPSOs, production capacity is forecasted to reach 560,000 barrels per day (bpd).

Natural Resource Fund

Profit oil accounted for thirteen (13) lifts of 1-million-barrel oil cargoes in the year 2022 in comparison with five (5) lifts for 2021. Profit oil amounted to G$262 billion and royalty amounted to G$32.2 billion for the year ended December 2022. The total assets of the NRF stood at G$298 billion as of the end of 2022.

Variance Between NRF and Financial Statements

Readers will observe that in the analysis presented, there is a notable variance between the profit oil and royalty reported in the Natural Resource Fund (NRF) versus the same as per the consolidated financial statements for 2022 when the fiscal formula is applied.

To this end, the average price of crude oil in 2022 that applied to the government’s share of profit oil and royalty was US$99.8 per barrel. However, it can be extrapolated that the financial statements of EEPGL, Hess and CNOOC for 2022 was prepared based on an average price of US$90.5 per barrel.

Hence, this partially explains the variance between the profit oil and royalty reported in the audited financial statements for the NRF when compared to the consolidated financial statements for EEPGL, Hess and CNOOC.

The other factor that would have contributed to the variance is the difference in exchange rates used for the conversion of USD/GYD by the Bank of Guyana, which was at a rate of $208.43, and whereas the average market exchange rate was at a rate of $207.76.

Author’s Calculation

Guyana’s net take inclusive of local content spend together with the government’s take cumulatively as of 2022 amounted to G$697.7 billion or US$3.34 billion representing 34.3% of the cumulative net operating cash flow for the period FY 2019-FY 2022―which stood at G$2.033 trillion or US$9.8 billion. Of this amount, the cumulative net cash flow transferred to the parent companies as repayment of initial equity capital invested amounted to G$6.4 billion or US$30 million representing 0.31% of the cumulative net operating cash flows for the period.

With the aforementioned in mind, this means that effectively the oil companies are reinvesting almost 100% of the net cash flows generated from the operating activities in Guyana in new exploration activities and to develop future projects into production. This is especially important since there is a limited window in which to extract these resources in view of the global energy transition agenda that is likely to have an impact on global demand for crude and ultimately resulting in lower crude oil prices in the future. And equally, it is crucial for Guyana to maintain the current pace and momentum in the industry aimed at enabling the country’s sustainable economic transformation and development agenda.

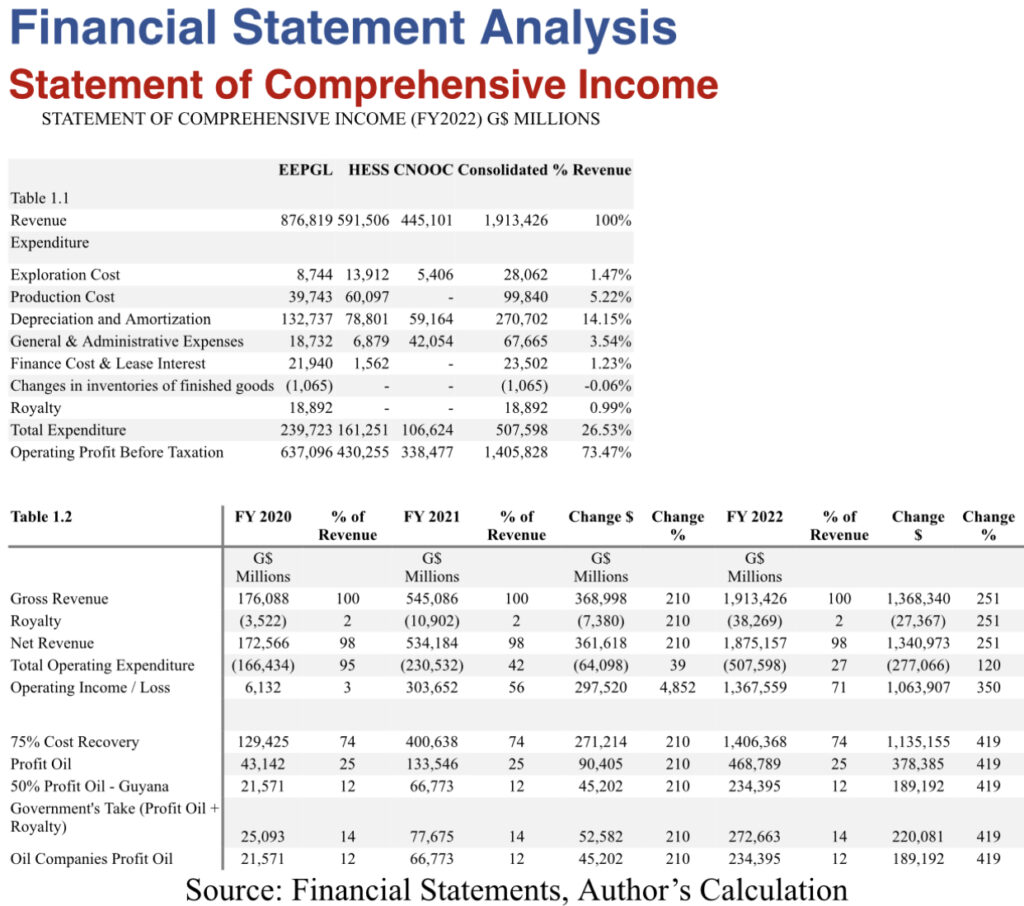

The consolidated statement of comprehensive income for EEPGL, Hess and CNOOC revealed gross revenue for FY 2022 at G$1.9 trillion or US$9.15 billion, representing an increase of G$1.36 trillion or 251% over the previous year. Operating expenditure amounted to G$507.9 billion and represented 26.53% of gross revenue, down from 42% of gross revenue in FY 2021.

Operating income before tax for FY 2022 amounted to G$1.4 trillion or US$6.7 billion, reflecting an increase of 350% or G$1 trillion over the previous year. However, by virtue of applying the fiscal formula in accordance with the terms and conditions of the PSA for the Stabroek block, the net operating profit amounted to G$234.4 billion or US$1.12 billion for EEPGL, Hess and CNOOC, while profit oil and royalty amounted to $272.6 billion or US$1.3 billion for the Government of Guyana (GoG). Consequently, the Government’s take is G$38.2 billion more than the net operating profit earned by EEPGL, Hess and CNOOC.

The consolidated statement of cash flow analysis for FY 2022 revealed that the net cash flows generated from operating activities amounted to G$1.552 trillion, the net cash outflows from investing activities amounted to G$812 billion and the net cash outflows from financing activities amounted to G$754.9 billion. Thus, with an opening cash balance for the period of G$18.5 billion, the net cash and cash equivalents as at the end of FY 2022, amounted to G$3.29 billion.

Having examined the cumulative statement of cash flows for the period FY 2019 to FY 2022, the cumulative operating income for the period amounted to G$1.693 trillion. Notably, for the years 2019 and 2020, cumulative losses were reported of G$25.8 billion.

The cumulative net cash inflows from operating activities amounted to G$2.033 trillion for the period or US$9.8 billion. The net cumulative cash outflows from investing activities amounted to G$2.033 trillion, and the cumulative net cash outflows from financing activities for the period amounted to $6.441 billion or US$31 million.

Importantly, it must be noted that the net cash outflows from the investing activities are essentially the cash outflows reinvested in Guyana for both exploration activities and development of new projects for production within the Stabroek block.

Whereas the net cash outflows from financing activities represents the cash flows remitted to the parent companies, representing repayment of invested capital contributed by the parent companies.

As such, the oil companies reinvest 99.69% of their net operating cash flows and profits into the Guyana market as previously explained. This means that less than 1% of the net operating cash flows from Guyana is utilized for dividend payments to shareholders by the parent companies.

The lack of ring fencing in respect of the fiscal framework was one of the main criticisms at the outset of the renegotiated Stabroek block PSA. The ring-fencing requirement is typically applied to oil and gas fiscal regimes with income taxes as part of the fiscal framework. In the case of Guyana, the Stabroek block PSA does not have an income tax component, per se, save an except for a nominal corporate tax.

Thus, the ring-fencing provision, for this reason, is not necessarily applicable because its purpose is usually to determine the taxable income in a given fiscal year.

In hindsight, there is another important dimension that stakeholders should consider wherein the lack of ring fencing is an incentive favorable to Guyana. With the imposition of ring fencing, the cost of capital would have been higher than the current cost of capital and it would have restricted the current fast-paced development of future projects.

To this end, the lack of ring fencing is enabling future projects to be financed from the cash flows generated from Guyana’s operations, which is cheaper, versus sourcing capital from shareholders’ equity and employing higher levels of debt financing which would be more expensive as well.

The local media, many local and external analysts and industry observers held the view that the Guyana market accounts for a substantial portion of EEPGL’s parent company’s net earnings globally. However, the illustration in the analysis herein confirms that this is not the case, which is an important perspective for the Guyanese stakeholders.

In this regard, EEPGL’s parent company, namely ExxonMobil’s comprehensive income for FY 2022 amounted to US$56.234 billion of which EEPGL’s comprehensive earning for the period amounted to US$522 million, thereby representing 0.93% of ExxonMobil’s global net earnings. Also, the net cash flows from operating activities of EEPGL represents 4.6% of the net cash flows of the parent company; the total assets of EEPGL represents 2.93% of the parent company’s total assets; and the cash and cash equivalents as of the end of year for EEGL represents 0.05% of the parent company’s cash and cash equivalents at the end of year.

3. Concluding Remarks

Overall, the analysis invalidates the following contrary views of other analysts and political commentators where:

i) EEPGL and its co-ventures raked three times more profit than Guyana for the period FY 2020–FY 2022, and

ii) That the oil companies and the government are united in keeping cost recovery numbers hidden according to one local media report.

About the Author

Joel Bhagwandin is a public policy/financial analyst―and an experienced financial professional with more than fifteen years’ experience in the financial sector, corporate finance, financial management, consulting, and academia.

He is actively engaged in providing insights and analyses on a range of public policy, economic and finance issues in Guyana over the last six years. He has authored more than 300 articles covering a variety of thematic areas.

Joel has also written extensively on the oil and gas sector. (Author’s professional profile on LinkedIn can be accessed here: https://www.linkedin.com/in/joel-bhagwandin-57481470/.)

{kind=link}