Highlights

There is no substantial depreciation or appreciation of the Guyana dollar; there is, however, fluctuation of the exchange rate which is a consequence of market forces. Notwithstanding, the exchange rate remains relatively stable.

The current monetary and exchange rate policy framework of exchange rate stability remains the most suitable at this time.

The foregoing is especially important considering the risks―should there be a change in relative prices; this could be detrimental to the non-oil export sectors whereby those sectors could become internationally uncompetitive.

The commercial banks, owing to the fact that they are the dominant players in the forex market, tend to manipulate the exchange rate to some extent, but not to the detriment of the macroeconomy.

The country’s net foreign sector assets and reserves comprising of the Natural Resource Fund (NRF) balance, the Bank of Guyana Net International Reserves, and the Commercial Banks’ Net Foreign Sector Assets, stood at US$2.636 billion at the end of 2022, representing 1.7 times the country’s external debt.

Introduction

In this article, I have opted to deviate a bit from the series which I started two weeks ago examining the performance of each sector and the efficacy of government policy together with the allocation of resources. Instead, I would like to address another issue in respect of the foreign exchange (forex) market, a seemingly emerging debate about exchange rate appreciation and depreciation by certain sections of the media. Several commentators have weighed in on the topic arguing for the revaluation of Guyanese currency. Recently, one writer (Peeping Tom column of August 29th, 2023) posited that the Guyanese currency is depreciatingrelative to the United States (U.S) dollar. The author argued that the “weakening of the Guyana dollar amidst the influx of oil revenues could raise concerns about Guyana’s financial stability”.

Discussion and Analysis

First and foremost, exchange rate stability is of paramount importance for the economy at this point in time. As such, the monetary policy stance of the central bank is geared towards ensuring that exchange rate stability prevails.

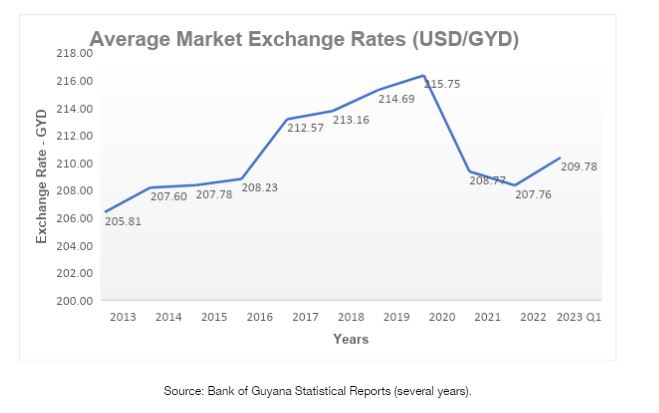

Secondly, the central bank operates a floating exchange rate regime, which means that there will be fluctuation of the exchange rate based on demand and supply. While this is rather normal, in the context of exchange rate stability, it is the degree of the fluctuation that matters. This is demonstrated in the chart hereunder.

Given that the commercial banks are the dominant players in the forex market, it is prudent to analyze the average market exchange rates of the commercial banks. By and large, the average market exchange rate has been stable over the last fifteen years, thus enabling macroeconomic stability. During the period 2015-2020, the exchange rate depreciated by $7.97 or 3.8%. Conversely, for the period 2021-2022, the exchange rate appreciated by almost the same level of 3.8%, thereby reverting to its pre-2015 level. In the first quarter of 2023, the exchange rate depreciated marginally by 0.97%.

These movements in the exchange rate are not to a great extent and is consistent with the fluctuation based on market forces as stated earlier.

It can also be argued that the commercial banks, owing to the fact that they are the dominant players in the forex market, tend to manipulate the exchange rate to some extent, as demonstrated below.

Table 1 (a) attached shows commercial banks forex activities for the period 2012-2022 and Q1 of 2023, including forex intervention in the market by the central bank. For the period 2012-2016, the central bank closed each fiscal year with a net sales position to the commercial banks. This means that the central bank injected forex in the market to ensure adequate supply of forex based on aggregate demand, whilst maintaining the stability of the exchange rate. For the period 2017–2022, the inverse of this situation occurred, wherein the central bank closed each fiscal year for that period, with a net purchase position from the commercial banks. This means that the commercial banks had excess foreign exchange in the system, which the central bank “mopped-up” from the market, to maintain a relatively stable exchange rate. In Q1 of 2023, when the exchange rate depreciated marginally by 0.97%, the central bank had a net sales position with the commercial banks, meaning that the central bank had to inject forex into the market.

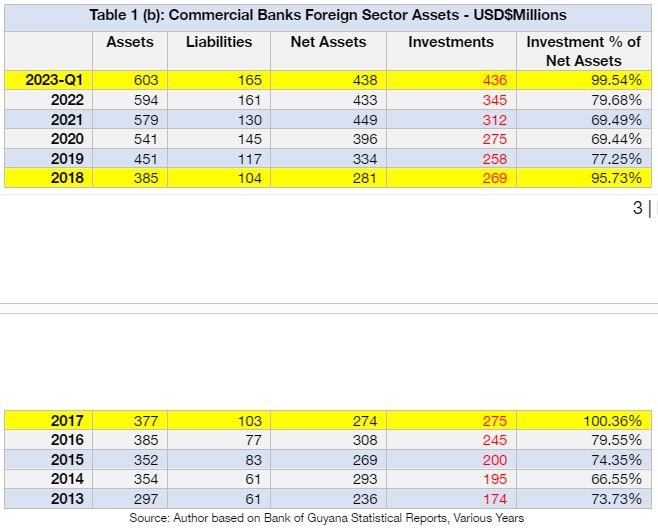

Table 1 (b) illustrates how the commercial banks effectively manipulate the exchange rate, which in turn creates a temporary disequilibrium in the market. But at the same time, it is important to understand why this is not to the detriment of the economy on a macro level. In fact, it is helping to protect the stability of the economy at the macroeconomic level, inter alia, staving off the Dutch disease.

Towards this end, as shown in table 1 (b), the net foreign assets of the commercial banks almost doubled over the last decade, from US$236 million in 2013 to US$438 million by the end of the first quarter in 2023. With these large, accumulated forex balances, the commercial banks have, over the years been allowed to prudently invest a portion of same in the regional and international financial markets. These include government treasury bills or sovereign bonds, securities, and commercial papers. As can be seen in the above table, the commercial banks have typically invested around 70%-80% of their net foreign assets in these instruments. In some instances, they have engaged in excessive exposure by investing as high as 95%-99% of their net foreign assets. Consequently, this creates a temporary disequilibrium in the market coupled with the normal transactional demand within the domestic market.

In that regard, if the commercial banks limit their exposure to not exceed 70%-80% of their net foreign sector assets; this would minimize the disequilibrium in the market that occurs from time to time. Additionally, in so doing it would help to restrict the fluctuation in exchange rate movement to within a certain level. For example, as illustrated in the chart above, the exchange rate had depreciated by 3.8% during the period 2017-2020. As a result, the central bank intervened by instructing both the commercial banks and non-bank cambios to limit the spread between the buying and selling rates to $3 dollars. There are other considerations for limiting the financial sector’s overseas exposure―such as the market and political risks of other countries. Nonetheless, there is no major threat currently considering the effects on the non-oil export sectors if there is a change in relative prices attributed to a substantial appreciation of the exchange rate (Dutch disease).

In an IMF Working paper titled “managing Guyana’s oil wealth: monetary and exchange rate policy considerations”, the paper contends that the current de facto monetary policy framework, focused on exchange rate stability, is more suitable for Guyana at this point in time. The author argued that this is primarily because the exchange rate serves well as the nominal anchor for price stability. Moreover, the effectiveness of as an instrument for absorbing external shocks and balance of payment pressures. The author concluded that as “Guyana becomes a major oil producer over the medium to long-term, there is a strong case for revising the monetary and exchange rate policy framework since a gradual shift towards greater exchange rate flexibility will allow the economy to better withstand shocks and maintain competitiveness”. The IMF’s analysis correctly reflects the current situation and is consistent with the analysis presented herein.

It is worth noting that the country’s net foreign sector assets comprising of the Natural Resource Fund (NRF) balance, the Bank of Guyana Net International Reserves, and the Commercial Banks’ Net Foreign Sector Assets, stood at US$2.636 billion at the end of 2022, representing 1.7 times the country’s external debt (see table 2 below).

This is demonstrative of the fact that the country’s foreign sector assets and reserve position continue to grow due to the earnings from the oil and gas industry together with increased economic activities across all sectors.

Concluding Remarks

There is no major depreciation or appreciation of the Guyana dollar; there is, however, fluctuation in the exchange rate which is a consequence of market forces. The current monetary and exchange rate policy framework of exchange rate stability remains the most suitable at this time.

This is especially important considering the risks should there be a change in relative prices; this is likely to be detrimental to the non-oil export sectors, whereby those sectors risk becoming uncompetitive.

ABOUT THE AUTHOR

Joel Bhagwandin, MSc., is the Director of Financial Advisory, Market Intelligence, and Analytics at SphereX Professional Services Inc. He can be reached at [[email protected]](mailto:[email protected] “”).

{kind=link}