")

ExxonMobil, Chevron, Total S.A, and British Petroleum (BP), four of the world’s largest oil producers, have been spending beyond their means even as losses continue to increase during the COVID-19 pandemic. Making this disclosure in one of its latest reports today was the Institute for Energy Economics and Financial Analysis (IEEFA). This organization conducts research and analyses on financial and economic issues related to energy and the environment.

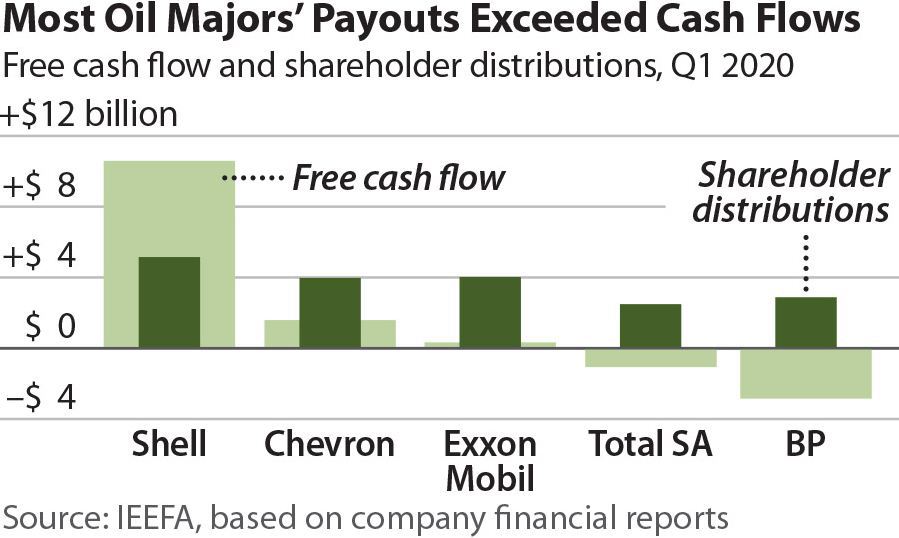

In its report , the Institute said that named companies spent more cash on dividends and share buybacks during the first quarter of the year than they generated from their core business operations. It was noted that the five oil and gas supermajors collectively paid out US$18.5 billion in dividends and buybacks during the quarter, while generating only US$8.6 billion in free cash flows. The companies covered the US$9.9 billion shortfall with other sources of cash, including borrowing, asset sales, and drawdowns of cash reserves.

Further findings showed that two of the companies – BP and Total ‒ spent more during the first quarter on capital projects than they received from operations, yet still paid dividends to shareholders. In the case of Chevron and ExxonMobil, these two companies reported modest positive free cash flows in the first quarter, but paid out far more to shareholders, making up the deficit with cash from other sources. According to the Institute, Royal Dutch Shell was the only oil supermajor to stay in the black. The company generated US$10.6 billion in cash from the oil and gas business while spending US$5.2 billion on dividends and share buybacks during the quarter.

Additionally, the IEEFA analysis found that the five supermajors—ExxonMobil, Chevron, Shell, BP and Total SA—have been spending beyond their means for much of the past decade. Together, the companies generated cumulative free cash flows of US$340 billion from the beginning of 2010 through the end of 2019, while spending US$556 billion on dividends and buybacks, resulting in a net deficit of US$216 billion.

Clark Williams-Derry who serves as an IEEFA Energy Finance Analyst was keen to note that typically, investors expect private companies to fund payments to shareholders out of free cash flow—the cash generated by the company’s operations, minus cash spent on capital projects. Williams-Derry said when a company deviates from this standard, investors raise questions about the firm’s business model, applying extra scrutiny to its financial underpinnings.

{kind=link}