Dear Editor,

Reference is made to Prof. C. Kenrick Hunte’s letter in the Kaieteur News edition of July 13, 2023, with the caption “EEPGL a ploy to plunder oil” (https://www.kaieteurnewsonline.com/2023/07/13/eepgl-a-ploy-to-plunder-oil/).

I would like to remind your readers that the goodly professor has many questions to answer to the Guyanese people in respect of his stewardship of GAIBANK. He was the last General Manager of GAIBANK and was largely responsible for the financial failure of that institution. Ironically, an appropriate description of his management performance therein would be one that is akin to the very description he ascribed to EEPGL.

The learned professor continues to rely on secondary reports with various pieces of information, which he then uses to perform extrapolatory analysis. This technique, in the absence of him utilizing the actual financial information reported in EEPGL’s and its Co-ventures financial statements, renders the professor’s analysis inaccurate. Since his letters are regularly published by Kaieteur News, I urge him to request the financial statements from that media entity and perform a proper financial analysis.

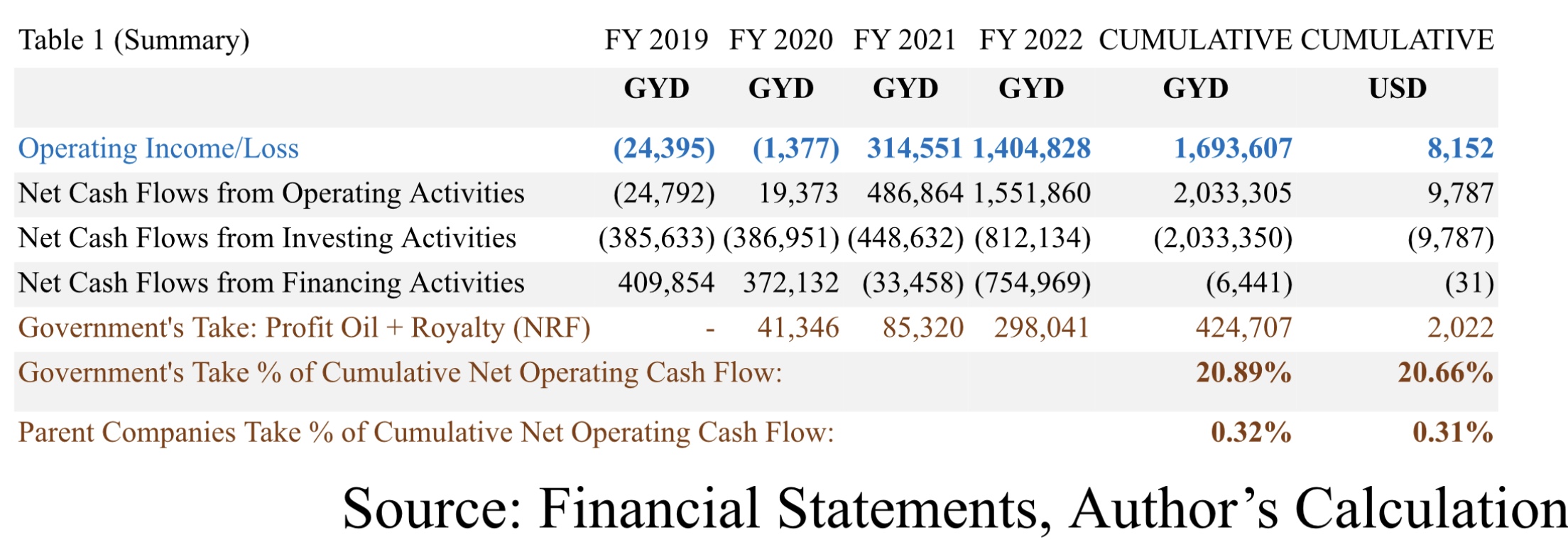

With that said, in his letter, he argued that EEPGL recovered all of its investment, and he cited a number of US$4.4 billion as the initial investment from a revenue of US$14.08 billion. The professor’s initial investment figure is incorrect. That initial investment is for the Liza One development alone and pre-exploration cost. He ignored the development and exploration costs for Liza Two, Payara, Yellowtail and the others. Clearly, he does not understand the financing structure for these developments. So, let’s look at the statement of cash flow analysis for FY 2022 as seen in the chart attached.

The consolidated statement of cash flow analysis for FY 2022 revealed that the net cash flow generated from operating activities amounted to G$1.552 trillion, the net cash outflow from investing activities amounted to G$812 billion and the net cash outflow from financing activities amounted to G$754.9 billion. Thus, with an opening cash balance for the period of G$18.5 billion, the net cash and cash equivalents as at the end of FY 2022, amounted to G$3.29 billion.

Having examined the cumulative statement of cash flow for the period FY 2019 to FY 2022, the cumulative operating income for the period amounted to G$1.693 trillion. Notably, FY 2019 and FY 2020, cumulative losses were reported of G$25.8 billion. The cumulative net cash inflows from operating activities amounted to G$2.033 trillion for the period or US$9.8 billion. The net cumulative cash outflows from investing activities amounted to G$2.033 trillion, and the cumulative net cash outflows from financing activities for the period amounted to $6.441 billion or US$31 million. Importantly, it must be noted that the net cash outflow from the investing activities are essentially the cash outflow reinvested in Guyana for both exploration activities and development of new projects for production within the Stabroek block. Whereas the net cash outflows from financing activities represents the cash flows remitted to the parent companies, representing repayment of invested capital contributed by the parent companies.

With the foregoing in mind, the oil companies reinvest 99.69% of their net operating cash flow and profit into the Guyana market to develop future projects within the Stabroek block, recovery of their initial investments, and to fund new exploration activities. This means that less than one percent of the cash flow from Guyana is utilized for dividend payments to shareholders. Noteworthily, the cumulative net cash flow from profit oil and royalties that the government earned for the period amounted to G$424.7 billion or US$2 billion, represents 20.66% cumulative net cash flow from operating activities. Conversely, the oil companies’ net earnings paid to their parent companies for the period which amounted to G$6.44 billion or US$31 million, represents 0.31% of the cumulative net operating cash flow for the period. Clearly, this is substantially lower than the cumulative sum that the Government earned in profit oil and royalties.

The foregoing analysis simply demonstrates that the oil and gas exploration, development, and production activities in Guyana, is financed in large part from the shareholders’ equity (initial capital), cash flow from operations, and a small portion of debt financing (30%). Therefore, the notion that EEPGL has recovered all of its invested capital and is plundering the profits, is woefully misleading.

Yours respectfully,

Joel Bhagwandin

{kind=link}