Dear Editor,

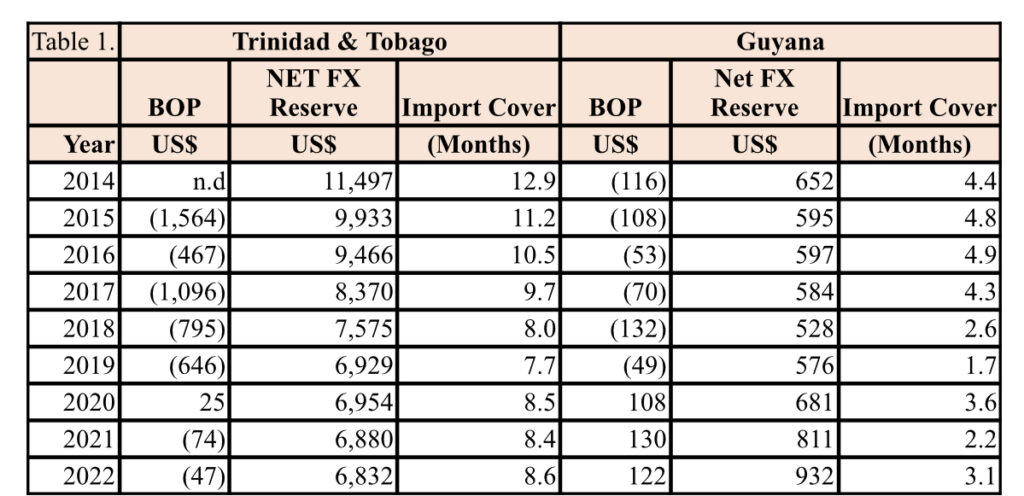

My attention was drawn to a statement made by Trinidad & Tobago’s (T&T) High Commissioner to Guyana, Ambassador Conrad Enill. In his statement, he asserted that there is no shortage of foreign currency (forex) in T&T in response to claims made by Guyana’s Vice President, Dr. Bharrat Jagdeo. To substantiate his claim, the Ambassador went onto state that Guyana’s foreign reserve is equivalent to 1.4 months import cover whereas T&T is the equivalent of 8.6 months import cover as of the end of 2022.

However, the Ambassador’s figure for Guyana is incorrect. The fact is that Guyana’s foreign reserve has improved since the PPP/C Government has been re-elected in 2020, which was below 2 months import cover during that period but has improved to 3 months import cover at the end of 2022.

As shown in table one above, in 2014 T&T net forex reserves stood at US$11.5 billion which represented 12.9 months import cover. By the end of 2022, the forex reserves declined by US$4.665 billion to US$6.8 billion, the equivalent of 8.6 months import cover. In the case of Guyana, for the same period, in 2014 the forex reserve stood at US$652 million representing 4.4 months import cover, which fell below 3 months import cover during the period 2018-2019, and in 2021. At the end of 2022, the forex reserves increased to US$932 million, up from 2.2 months import cover in 2021 to 3.1 months import cover.

Readers would recall that in my previous essay on this matter, I pointed out that T&T and Guyana operate two different exchange rate regime. In this regard, T&T operates a fixed exchange rate regime, inter alia, enforcing strict exchange rate controls especially at times when the country’s forex reserves is depleting at an alarming rate.

Typically, countries with fixed exchange rate system usually set the exchange rate at a level that overvalues the local currency. The disadvantages with this type of exchange rate system, which T&T is experiencing for the past seven years or so, are that:

i) the situation is not tenable indefinitely, foreign reserves dwindle fast,

ii) the only way to sustain this system is to implement controls, and

iii) the private market usually responds with an illegal or parallel currency market.

The situation described at (iii) above may have been contained, because T&T companies that are operating in other markets such as Guyana, have been sourcing forex from those markets, and this has been confirmed by the Guyanese authorities.

With that in mind, T&T may not have a forex shortage in a real sense at the moment―from the perspective of the level of the country’s net forex reserve relative to their import cover. Nonetheless, they do have a serious problem wherein the forex reserve has been depleting at a relatively fast rate, which could culminate into an economic crisis in a few years’ time.

The current economic situation in T&T can be partially explained by the external trade data in the above table. Energy exports accounts for 80-86% of total exports. Since 2015, energy exports amounted to US$9 billion, which fell below this amount in 2016-2017, rebound to 2015 level in 2018, and fell below that level again in 2019 through 2021, recording its lowest level at US$4.3 billion during the period. The non-energy exports also fell below the 2015 level of US$2.6 billion to less than US$2 billion from 2016 – 2020, then rebound to just over $2 billion in 2021-2022, but less than where it was in 2015. This outturn is indicative of T&T’s failure to adequately diversify the non-oil economy, hence their heavy reliance on the energy sector, despite being an oil and gas producing economy for over a century.

On the other hand, Guyana is keen to avoid this in the long term, viz-a-viz, the government’s commitment to execute an aggressive, expansive development agenda aimed at diversifying the non-oil economy.

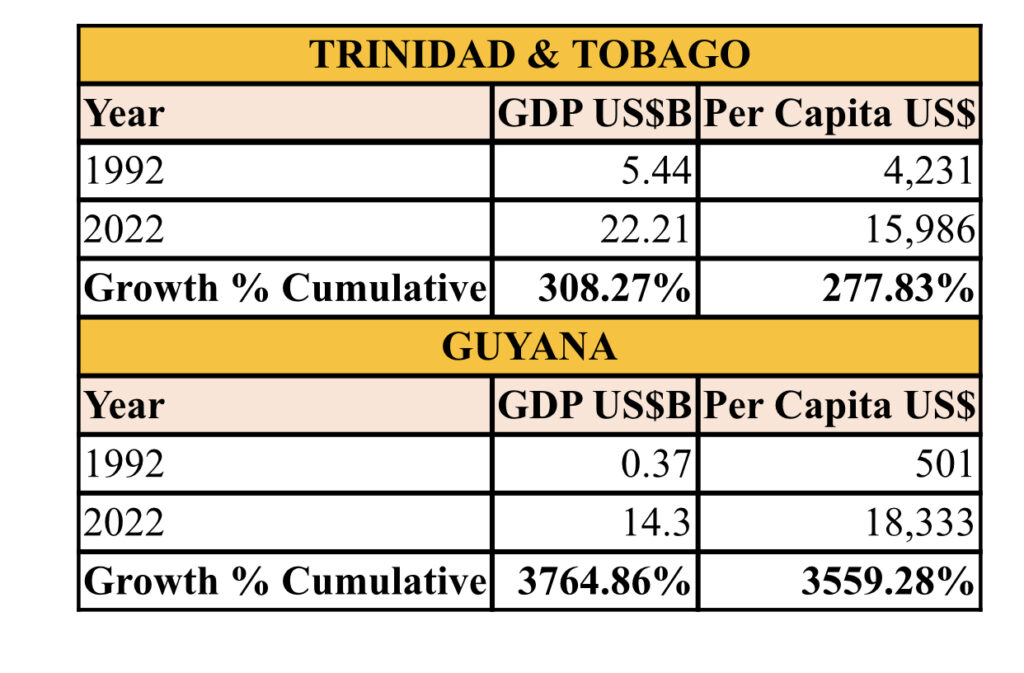

Table 3 below illustrates an interesting perspective, whereby for the period 1992-2022, Guyana has outperformed the T&T economy by almost 35 times over.

In 1992, T&T’s GDP stood at US$5.44 billion with a per capita income of US$4,231, which increased by 308.27% to reach US$22.21 billion, and 277.83% to reach US$15,986 respectively, by the end of 2022.

For the same period, spanning three decades, Guyana’s GDP stood at US$370 million and per capita income was US$500 in 1992. Bearing in mind that Guyana was a bankrupt economy at that time, which T&T helped by generously writing off Guyana’s debt with T&T at that time, in an effort to reduce the debt burden. By the end of 2022, real GDP increased cumulatively by 3,764.86% to reach US$14.3 billion, and per capita income increased cumulatively by 3,559.28% to reach US$18,333, surpassing T&T’s per capita income of US$15,986 in 2022.

Finally, Guyana is poised to become the economic backbone of the region, a role that T&T carried for decades. It is crucial, therefore, that T&T recognizes this as a positive development and position itself to work with Guyana and the rest of the region. In this regard, Guyana still needs tremendous amount of support to develop its own resources in terms of human, physical, technological, financial, and its capacity, to effectively pursue its development goals. Herein lies the opportunity for T&T to assert itself as a strategic partner to advance the economic prosperity of both countries.

Yours respectfully,

Joel Bhagwandin

Financial Analyst

{kind=link}